Gold loans have become one of the most preferred financial tools in India, especially during times of urgent need. With the increasing demand and involvement of various financial institutions, the Reserve Bank of India (RBI) recently released a set of draft guidelines aimed at creating a more secure, transparent, and uniform system for gold loan practices.

In this blog, we’ll break down these new RBI proposals in a simple and easy-to-understand manner, explaining what changes are coming and how they impact both borrowers and lenders.

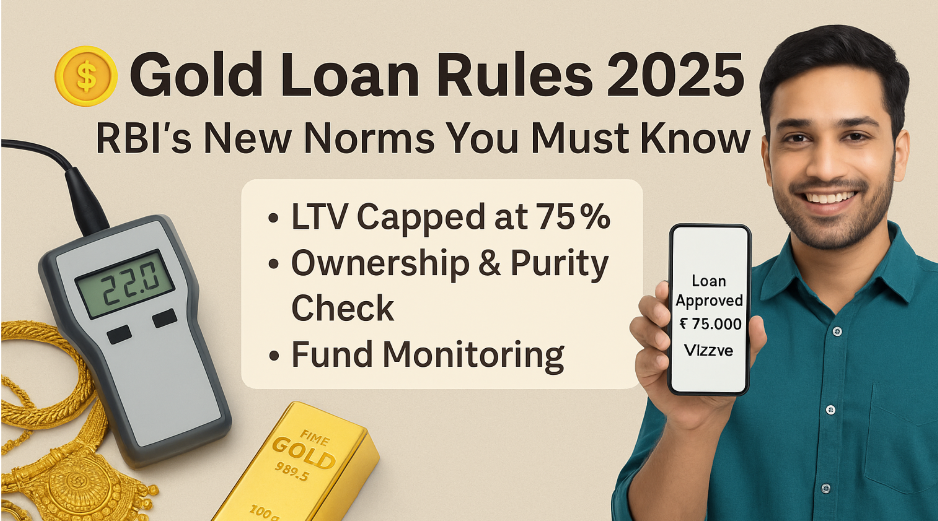

1. Loan-to-Value (LTV) Ratio Capped at 75%

One of the most important changes is that all gold loans will now have a fixed loan-to-value ratio of 75%. This means that no matter where you borrow from – a bank or a non-banking financial company (NBFC) – the loan amount cannot exceed 75% of the current value of your gold. This cap is especially relevant for bullet repayment loans, where the entire amount is paid back at the end of the term.

This change is designed to control risk for lenders while ensuring that borrowers don’t end up over-borrowing based on inflated gold prices.

2. Clear Ownership and Collateral Rules

Gold loans will only be allowed against gold owned by the borrower. Lenders must verify that the gold being pledged is indeed the borrower’s property. This rule helps eliminate any chance of fraudulent pledging and ensures fair play for everyone involved.

3. Standardized Gold Valuation

To avoid confusion and inconsistencies, all lenders are now required to follow a uniform process when assessing the purity and weight of gold. Only trained and certified professionals should handle this task, ensuring that the borrower gets the right value for their gold.

4. Monitoring How the Loan Is Used

Lenders will now keep a closer watch on how the loan money is being used. Borrowers might be asked to provide a basic idea of how they plan to use the funds. This is especially important for larger loans, where the end-use must align with legal and ethical financial practices.

5. Restrictions on Acceptable Gold Collateral

The new guidelines also limit the type of gold that can be pledged. For example, gold-backed financial products like mutual funds or ETFs are no longer allowed as security. Only specific types of gold, like 22-carat coins sold by banks or actual jewelry, are permitted.

This rule helps ensure that the collateral is tangible and easier to value and recover in case of default.

6. Loan Limits and Tenure

There are also clear rules about how much you can borrow and for how long. For bullet repayment loans, the term cannot exceed 12 months. Cooperative banks and rural banks can only offer gold loans up to ₹5 lakh per borrower. Additionally, there is a weight limit on the gold that can be pledged – not more than 1 kg in total and 50 grams for coins.

This ensures responsible borrowing and lending, especially in rural and semi-urban areas where gold loans are more common.

7. Faster Return of Gold Post Repayment

One of the borrower-friendly aspects of these guidelines is the mandate for lenders to return the pledged gold within seven working days after the loan is fully repaid. If there is a delay, the lender is liable to pay a penalty of ₹5,000 for each day of delay.

This move is a major relief for borrowers who worry about unnecessary delays in getting their gold back.

8. Transparent Auctions in Case of Default

If a borrower defaults and the lender needs to sell the gold, the auction process must be completely transparent. The borrower should be informed in advance, and the auction should be publicized through regional and national newspapers. Any amount received over and above the outstanding loan must be returned to the borrower.

This ensures that even in cases of default, the process remains fair and ethical.

9. Detailed Borrower Assessment

Before approving a gold loan, lenders are now required to assess the borrower’s ability to repay. This includes reviewing income, past loan history, and other financial aspects.

The idea is to prevent people from falling into a debt trap and to promote responsible lending.

Final Thoughts

The RBI’s new draft guidelines are a strong step toward streamlining gold loan practices across India. They not only promote fairness and consistency but also protect both borrowers and financial institutions.

For borrowers, these changes bring better transparency, quicker processing, and increased protection. For lenders, they offer a more structured and secure way to manage gold loans. As the gold loan market continues to grow, these rules will help build a stronger and more trustworthy system for everyone involved.

“This Content Sponsored by Buymote Shopping app

BuyMote E-Shopping Application is One of the Online Shopping App

Now Available on Play Store & App Store (Buymote E-Shopping)

Click Below Link and Install Application: https://buymote.shop/links/0f5993744a9213079a6b53e8

Sponsor Content: #buymote #buymoteeshopping #buymoteonline #buymoteshopping #buymoteapplication”